Window of Weakness

- We believe the global economy is about to enter a low-growth “window of weakness,” a period we expect to persist into 2020.

- In our baseline forecast, the low-growth period of vulnerability over the next several quarters gives way to a moderate recovery in U.S. and global growth in the course of 2020.

- However, our conviction in this baseline economic narrative is lower than usual, given the environment of elevated political uncertainty and fat left and right tail risks.

- During this window of weakness, we think it prudent to focus on capital preservation, to be relatively light in taking top-down macro risk in portfolios, to be cautious on corporate credit and equities, to wait for more clarity, and to take advantage of opportunities as they present themselves.

In the four months since our annual Secular Forum, investors have been busy “Dealing With Disruption” (Secular Outlook, May 2019) – such as the escalating trade war between the U.S. and China, changes in government in the U.K. and Italy, the U.S. president criticizing the Federal Reserve, and the vertiginous plunge in bond yields in August.

Against this backdrop of political and market volatility, PIMCO’s investment professionals and advisors convened in Newport Beach in mid-September for our Cyclical Forum to reassess the macro outlook and our positioning for the next six to 12 months.

In a nutshell, we concluded that the global economy is about to enter a low-growth “window of weakness,” which we expect to persist going into 2020 with heightened uncertainty about whether it is a window to recovery or recession. During this window, we think it prudent to focus on capital preservation, to be relatively light in taking top-down macro risk in portfolios, to be cautious on corporate credit and equities, to wait for more clarity, and to take advantage of opportunities as they present themselves.

Slowing to stall speed

In our baseline scenario, we expect global GDP growth to slow further over the next several quarters as ongoing trade tensions and heightened political uncertainty in multiple jurisdictions continue to act as a drag on global trade, manufacturing activity, and business investment.

While labor markets have remained firm and consumer spending relatively solid in most advanced economies, we see the slump in global trade and manufacturing increasingly affecting other economic sectors via sagging corporate profits, reduced hiring, and a pullback in business investment. We expect U.S. GDP growth to slow to a meager 1% or so in the first half of 2020, down significantly from 3% in the first quarter and 2% in the second quarter of 2019. This would further corroborate our thesis that U.S. economic growth will be “Synching Lower” toward the rest of the world over the course of this year.

As a consequence, we see the global and the U.S. economy entering a low-growth window of weakness during which they are more vulnerable than usual to adverse shocks, with heightened uncertainty about whether it is a window to recovery or recession. While a recession is not our base case, it doesn’t take much to tip over an economy that is moving along at stall speed.

Fat left and right tails

In our baseline forecast, the low-growth period of vulnerability over the next several quarters gives way to a moderate recovery in U.S. and global growth in the course of 2020 in response to generally supportive fiscal policies and further monetary easing in both developed and emerging markets.

However, our conviction in this baseline economic narrative is lower than usual, given the environment of elevated political uncertainty and fat left and right tail risks. We see two main catalysts that could produce either better or worse economic outcomes than in our baseline.

The first major swing factor for the outlook is trade policy. On one hand, a further escalation of the trade war could easily tip an already slowing global economy into recession. On the other hand, a comprehensive trade deal between the U.S. and China that removes a significant portion of the already imposed and prospective tariff increases could produce a synchronized reacceleration of global growth in 2020. However, our base case is that while a limited trade deal is possible, the tensions between the U.S. and China are likely to remain on a low boil rather than cooling down permanently.

Monetary and fiscal policies are the other main swing factor that could push the economy and markets into left and right tail scenarios. Our base case is that the Fed, following the two rate cuts in July and September, delivers additional easing over the next several quarters, thus dis-inverting the U.S. Treasury yield curve and reducing recession risks.

However, given the apparent divisions within the Fed about the appropriate course of action, as well as some likely near-term upside for inflation as the tariffs pass through, there is a risk that the Fed under-delivers relative to market expectations. As the sell-off in risk assets during the fourth quarter of 2018 showed, markets are very sensitive to a more-hawkish-than-expected Fed. At our forum, we discussed the divergence between the inverted yield curve, which appears to price in significant recession risks, and tight credit spreads and elevated equity markets, which seem to suggest a more benign economic scenario. We concluded that the likely explanation is that risk markets expect aggressive Fed action to avert a recession and believe it will be successful. If so, a less-dovish-than-expected Fed risks sparking a significant tightening of financial conditions via a sell-off in equity, credit, and rates markets.

Conversely, the main upside risk to economic growth, apart from a comprehensive trade deal, is that fiscal policy in major economies becomes more expansionary. While our baseline foresees only moderate fiscal stimulus over the cyclical horizon, there is a chance that slowing growth and – in Europe and Japan – negative bond yields and “QE infinity” incentivize governments to become more proactive in supporting growth.

Investment implications

In looking at the investment implications of the cyclical window of weakness for the global economy, we note global rates markets price in recession-like conditions already, while corporate credit markets and risk markets more generally appear to price in better outcomes, either in terms of the macro outlook, the efficacy of central banks in continuing to supress volatility, or both.

In this environment we think it prudent to focus on capital preservation and to be relatively light on top-down macro risk positions in our portfolios, combined with a cautious approach on corporate credit. Given the uncertainty in the outlook – and the potential for right tail as well as left tail risk – we will wait for more clarity and will take advantage of opportunities as they present themselves, rather than placing a great deal of weight on our baseline outlook in our portfolio construction.

A slowdown or modest recession would not necessarily have a supersized impact on spread markets. However, following a long period of risk-seeking behavior and dip buying, we seek to protect portfolios against the risk of more significant market dislocation. We will maintain a very close focus on liquidity management.

Duration

On duration, the level of yields continues to look too low given our baseline outlook. That said, and notwithstanding the recent retracement, in the event that recession risk increases we see the potential for an ongoing global grab for duration that may be quite insensitive to yield levels. U.S. Treasury duration continues to look like the best source of “hard” duration to provide a hedge to risk assets in portfolios.

Overall, we expect to remain fairly close to neutral on duration across our investment strategies, depending on the other balance of positions in portfolios. Similarly, while we see a range of relative value opportunities, we do not have high top-down conviction on curve positioning.

Credit

We will remain cautious on corporate credit risk, reflecting both tight valuations at a time of above-average recession risk and our concerns over credit market structure: We’re closely watching the increase in corporate issuance and investment industry allocation to credit combined with the decline in dealer balance sheets for trading.

We favor “bend-but-don’t-break” credit (short-dated and default-remote) and will look to implement the high conviction ideas of our global team of credit analysts and portfolio managers. But we will be very wary of exposure to generic corporate credit at tight valuations.

We continue to see structured credit, notably U.S. non-agency mortgages and other residential mortgage-backed securities (RMBS), as offering relatively attractive valuation, a more defensive source of credit risk, and a less crowded sector.

Agency MBS and TIPS

We believe U.S. agency mortgage-backed securities (MBS), after recent poor performance, offer both reasonable valuation and carry, and we expect to be overweight. U.S. TIPS (Treasury Inflation-Protected Securities) also offer value in our view, again given recent underperformance, particularly in the context of our outlook for steadily rising U.S. core inflation and a Fed that weights downside macro and market risks much above inflation concerns currently.

Emerging markets

We favor modest emerging market (EM) currency overweights, with careful scaling of positions, based upon valuation and carry considerations. We also expect to find select opportunities in EM external and local markets.

Commodities

On commodities, our team has a neutral view overall, expecting the commodity markets to broadly follow macro developments. The team has a positive view on oil, based upon supply and demand dynamics, which have been reinforced by the disruption to Saudi Arabian production.

Equities

On equities, our asset allocation team sees downside risks to profit growth, and favors a modest underweight equity position in multi-asset portfolios with an ongoing emphasis on high quality defensive growth positions.

ESG

Finally, environmental, social, and governance (ESG) concerns remain crucial to our investment decision-making, both to target specific client objectives but also to strengthen our overall investment process.

Regional economic forecasts

2020 outlook for major economies

U.S.: A period of increased vulnerability

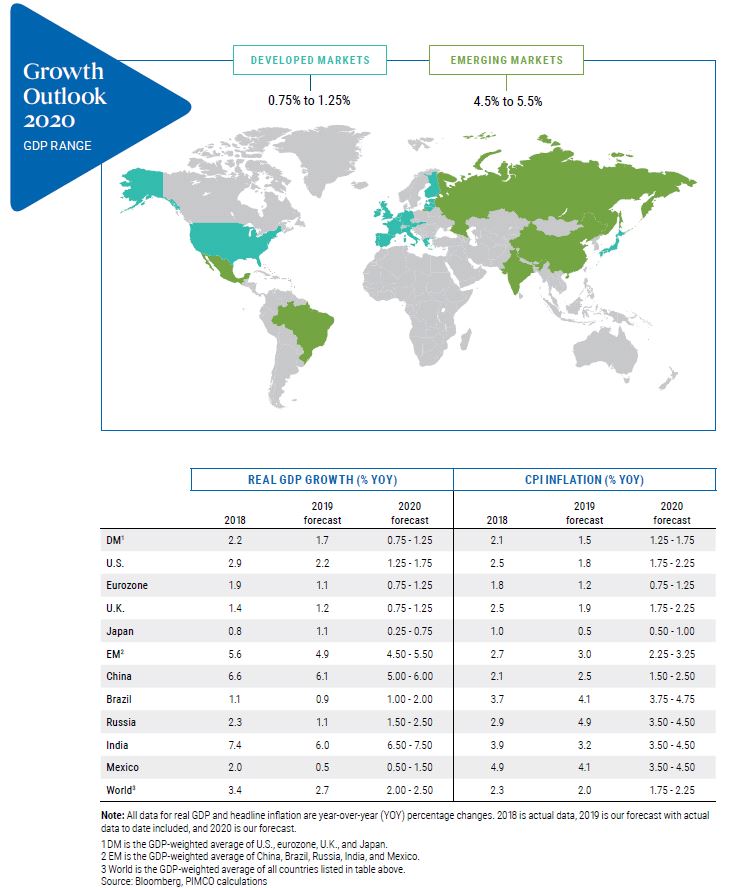

We expect real U.S. GDP growth to continue to slow to a 1.25% to 1.75% range in 2020, from a peak of 3.2% in the second quarter of 2018. The trend-like forecast for the entire year masks a sharper growth deceleration over the next few quarters, where we see the U.S. economy in a period of increased vulnerability. Slower global growth and elevated trade tensions are expected to continue to depress investment and export growth. Alongside this, we expect slower business output and lower profit growth will continue to slow labor markets, which in turn will tend to weigh on consumption somewhat.

With the recently implemented and announced tariffs on Chinese goods, we expect core consumer price inflation to firm somewhat further in the next few quarters, before moderating in the later part of 2020. Against this backdrop we expect the Fed to act to support growth and keep financial conditions anchored by cutting rates further over the next few quarters. The effects of Fed, as well as global government and central bank, policy actions to ease financial conditions, lower rates, and stimulate growth to counteract the slowdown underpin our forecast for some growth reacceleration in the second half of 2020.

Eurozone: The 1% economy

We see the continuation of a 1% growth, 1% inflation economy. Ongoing trade tensions will exert a significant drag on eurozone growth, somewhat offset by supportive domestic conditions, including easy financial conditions, some modest fiscal stimulus, and some remaining pent-up demand. Sequentially, growth is expected to improve modestly over the forecast horizon as trade conditions improve gradually through the year, but this remains uncertain.

We expect core eurozone inflation to remain low, close to the current level of around 1%. It could rise by a tenth or two over the cyclical horizon in response to rising wages, but weak growth suggests that margin pressure for businesses will remain in place, limiting the pass-through of higher labor costs into prices. At the margin, the weaker euro exchange rate should provide a modest lift to core goods’ prices.

While the European Central Bank potentially will cut the policy rate a little further, we would expect the focus to remain on forward guidance, TLTROs (targeted longer-term refinancing operations), and continued asset purchases.

U.K.: Deal or no deal

We expect an orderly form of Brexit over the cyclical horizon, either through an amended withdrawal agreement or a relatively orderly no-deal exit with side deals or stand-still arrangements in place, mitigating the short-run economic disruption. However, neither a chaotic no-deal nor a revocation of Brexit can be entirely ruled out, so while we have a stable baseline, we are mindful of left and right tail risks of outcomes worse or better than the central baseline.

In our baseline, we expect U.K. GDP growth of 0.75% to 1.25% in 2020, modestly below trend, as headwinds from weak global trade, Brexit-related uncertainty, and possible disturbances in the event of an orderly no-deal exit weigh on growth. Against that, a fiscal boost and resilient consumer will likely provide some support.

Meanwhile, we see core CPI inflation at or close to the 2% target. While wage growth has picked up, we do not expect it to meaningfully feed into higher consumer prices, with firms instead likely to absorb the higher labor costs in their profit margins. In this environment, we expect the Bank of England to keep its policy rate unchanged at 0.75%, but to cut in the event of a no-deal exit.

Japan: External headwinds

We expect GDP growth to slow to a 0.25% to 0.75% range in 2020 from an estimated 1.1% this year. We expect domestic demand to remain resilient thanks to a tight labor market and anticipated fiscal accommodation which would likely more than offset a negative impact of the consumption tax hike planned in October. However, the balance of risk remains on the downside as the Japanese economy faces headwinds from external factors.

Inflation is expected to remain low in a 0.5% to 1% range, with most of the impact from the consumption tax hike to be offset by lower mobile phone charges and free nursery education.

Policy-wise, “fiscal is the new monetary.” Monetary policy is at or close to exhaustion on a standalone basis, but there is clear appetite for fiscal stimulus from both the Bank of Japan and the government. Given external risks are materializing, the likelihood of Bank of Japan action is increasing; however, the hurdle for deeper negative rates remains high from a cost-benefit standpoint.

China: Using the yuan as an automatic stabilizer

We see GDP growth slowing into a 5.0% to 6.0% range in 2020, from an estimated 6.0% this year. The trade conflict escalated after the latest rounds of tariff increases, unemployment is rising, consumption is weakening, property investment has peaked, and business investment remains sluggish. Fiscal policy should provide a partial cushion: We expect fiscal stimulus of around 1.0% GDP for infrastructure and household consumption, likely front-loaded in the first quarter of 2020.

Consumer price inflation in China should remain benign around 1.5% to 2.5% after a temporary disease-related shock increase in pork prices as producer price disinflation is deepening and core inflation is weakening.

Policymakers have been using a flexible exchange rate as an automatic stabilizer. We expect further moderate yuan depreciation against the U.S. dollar as tariffs increase further. This should somewhat cushion the trade war’s impact on manufacturing. In addition, we expect the People’s Bank of China to cut rates by 50 basis points, in addition to reductions in banks’ reserve requirement ratios. However, credit conditions are likely to remain relatively tight and policy transmission slow due to rising defaults and shadow banking deleveraging.

Featured Participants

Disclosures

Past performance is not a guarantee or a reliable indicator of future results.

All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Sovereign securities are generally backed by the issuing government. Obligations of U.S. government agencies and authorities are supported by varying degrees, but are generally not backed by the full faith of the U.S. government. Portfolios that invest in such securities are not guaranteed and will fluctuate in value.

Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government-agency or private guarantor, there is no assurance that the guarantor will meet its obligations. Inflation-linked bonds (ILBs) issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. Treasury Inflation-Protected Securities (TIPS) are ILBs issued by the U.S. government. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be suitable for all investors. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Socially responsible investing is qualitative and subjective by nature, and there is no guarantee that the criteria utilized, or judgment exercised, by PIMCO will reflect the beliefs or values of any one particular investor. Information regarding responsible practices is obtained through voluntary or third-party reporting, which may not be accurate or complete, and PIMCO is dependent on such information to evaluate a company’s commitment to, or implementation of, responsible practices. Socially responsible norms differ by region. There is no assurance that the socially responsible investing strategy and techniques employed will be successful.

There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only. Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world. ©2023, PIMCO.