One Big Idea

Investing and business success can often depend on one BIG idea and its timing. The peaking of short-term interest rates at 20% in the early 1980s and the bursting of the DotCom and NASDAQ bubble 20 years later were excellent examples of big ideas that made or broke investment portfolios. A similar tale was told by the late Peter Bernstein as he recalled his early career in the 1950s when investing for income was rapidly becoming old hat, appropriate perhaps for widows and orphans, but not for red-blooded business executives focusing on a new era of growth. He writes that one client told him, “Please remember, I just can’t stand more income.” Back then, Bernstein suggests, income was for “sissies.”

In 2014, the tide may be turning again as demographics, fear of another Lehman, or just income-starved insurance companies and similarly structured liability-influenced institutions, reach for anything they can get. The era of income may be, at the margin, replacing the era of capital gains, despite artificially low current yields.

If so, the proper analysis of where to find high, yet relatively safe, income should be one of the top priorities of any investment management company. In addition to bottom-up credit analysis, the timing and ultimate destination of PIMCO’s New Neutral short-term interest rate thesis will be critical.

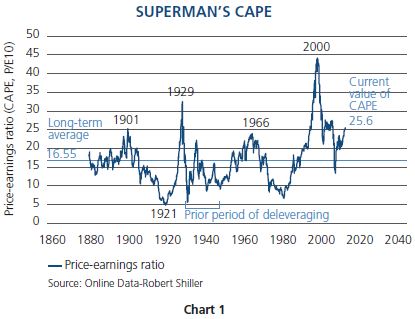

For example, if The New Neutral real FF (federal funds) rate is 0% instead of the Fed’s currently presumed 1¾%, then not only bonds but all financial assets might logically be repriced relative to historical experience. Even after accepting the historical validity and predictive capability of Robert Shiller’s CAPE (10-year cyclically adjusted P/E ratio), it may be necessary to make adjustments to it, if in fact real policy interest rates over the long term have settled into a lower New Neutral. At PIMCO, we are amazed that little outside analysis has been applied to this concept that to us affects the array of financial assets available to investors. One has only to apply Gordon’s dividend discount model to measure the potential effect that a 0% real policy rate would have on stock prices versus the presumed 1¾ - 2% of an “old normal.” P = D/R-G, states the Gordon model, with R in this case being the real rate of interest that may be substantially lower than prior levels. Ex-Fed Chairman Ben Bernanke has argued in private conversations that R is lower because G (growth) will be equally lower in future years. We agree, but would add that in a highly levered world, R has been and must remain reduced more than G in order to keep our financed-based economy functioning. If we are correct, Shiller’s CAPE may have to be adjusted from an historical median 17x P/E to something resembling 20-22x. That would not mean that today’s 16-multiple P/E market should be elevated to an immediate 20x, but that the current CAPE of 25x, as shown in Chart 1, is less bubbly than presumed. Fed officials who cite bubbly aspects of “financial conditions” should therefore be less alarmed. If the real New Neutral is significantly lower than 10 or 20 years ago, P/E ratios should be higher, credit spreads should be tighter, and home prices less bubbly than presumed if, in fact, The New Neutral is “neutral” and can lead to historical levels of asset volatility. The New Neutral is critical to future investment success. This currently is PIMCO’s “one big idea.”

The following is an excerpt from a recent speech given at the Morningstar Investor Conference in Chicago that more fully explains our logic concerning this New Neutral concept:

The New Neutral is simply the ‘biggest, most critical, most significant, most important’ element in asset pricing today. The policy rate, along with forward expectations, as well as volatility, corporate and equity risk premiums, has always provided the fundamental foundation for asset prices, aside (that is) from the inevitable bouts of exuberance and fear. But the neutral policy rate – in real and certainly nominal terms, changes over time. Irving Fisher back in the 1930s came up with the concept of a neutral policy rate, but he surmised it would change only with inflation. In other words, the real rate would be constant. History has proved otherwise. In the nearly 80 years since his theory was introduced, real policy rates have fluctuated from 0% to 8% during periods of positive inflation, and importantly, asset prices – bonds and stocks – have been significantly influenced by them. Do you wonder why stocks sold at P/Es of 6-7 times in 1981? Wonder no longer. It’s because nominal FF traded at 20%, and real FF at 7% or 8%. Equity risk premiums had to go up because real FF went up, which sent P/Es to what were rock bottom prices. Same thing with long Treasuries at 15%. It’s not that the market expected real funds to trade at 7-8% forever. But the forward path was exceedingly high, higher than Fisher could ever have imagined. For the next 30 years it came down, down, down and finally over the past few years real FF have been negative. 25 basis points nominal with 1.5% inflation has equaled a minus (1.25%) average real FF rate for much of the period.

So the real policy rate changes, and as Janet Yellen has recently agreed, there is an evolving neutral policy rate – a Goldilocks rate, which is “not too hot or not too cold, but just right” to promote Fed targets of 2% inflation and 3% real growth, which is nominal GDP of 5%. I might add, this neutral policy rate will now be expected to maintain moderate financial conditions and keep exuberance contained, an evolving third leg to Federal Reserve policy.

What is this real policy rate and is it really different than what we’ve seen for the past 25 years? Well, it’s likely not the current negative (1.25%), although that rate plus 1 trillion dollars of QE per year has been insufficient to generate 5% nominal GDP. What it has generated are what appear to some observers to be bubbly asset markets, and so perhaps they presume it must be raised to prevent popping. It will be, but by how much is the question. Nor, however, is the real rate likely to be 2% positive as markets experienced pre-Lehman. That was the rate embedded in the Taylor rule, formulated in the early ‘90s which worked quite well, until it didn’t, namely 2006–2007 when we had a real rate too high for a levered economy that it became the precursor to the Great Recession. The 2% Taylor real rate was a rate consistent with a significantly less levered financial economy than we have today. To return to a 2% real policy rate today would be to dice with another Lehman-like disaster. The real rate was only 1% at its peak before the financial system came tumbling down. It is almost comical to believe we can return to that point with our economy now levered 350% to GDP, much like it was five years ago. Although there is limited research beyond the Taylor Rule in this area, a 2001 San Francisco Fed Study by Laubach and Williams, which has been updated quarterly since, comes closest to the mark in my opinion. It suggests that The New Neutral should currently be a minus (25) basis points real, which would cap nominal FF at 1¾% if the Fed’s target of 2% inflation were to be reached. Other historical research by Rogoff & Reinhart covering the aftermath of the Great Depression and the 35 years-plus recovery into the 1970s, suggests real policy rates averaged a minus (25) to minus (100) basis points in the U.S. and the U.K. during this period. Deleveraging takes time and it takes very low real yields as well, it seems, to return an economy to Old Normal. It will likely take at least 5-10 more years before we approach the old Taylor model of 2% real, if then.

O.K., hopefully I haven’t put you to sleep. My point is that if The New Neutral is closer to 0% real than the Taylor 2% which many expect, then all asset markets, which are priced off of it, are less bubbly than they appear at the moment. P/Es of 16-17x seem reasonable with a 0% real policy rate. 10-year Treasuries at 2.60% do as well once a term premium is added to 2% inflation. Credit spreads themselves, while almost historically narrow, may be using the wrong history book IF Taylor is their guide. At 0% real, high yield spreads of 350-400 basis points make more sense as do other alternative asset yields. Collectively of course, all of these asset prices depend on Janet Yellen’s “not too hot, not too cold” assumption that produces at least 4% nominal GDP growth, but that of course is what Neutral means. Minsky and future Minsky moments have not been outlawed. It’s just that PIMCO believes the New rate is closer to 0% than 2%. If it’s closer to 2%, then bear markets in all asset classes await. We think not.

To PIMCO, this means that asset returns will be low, but less volatile than in prior periods. Perhaps that is why the VIX and Treasury volatility are so low currently. The market may be buying into PIMCO’s view of a slow crawl to a New Neutral. Admittedly, on the other side of the argument, I haven’t even discussed the levered global economy, China, Euroland, or other potential hot spots that might spark another flash crash and mass exodus. There is tail risk in a levered global economy both on the inflationary and the deflationary sides. We have been living with that risk for 5 years now and it will continue around the world, most visibly perhaps in Japan where deflation and inflation have suddenly come together like two giant galaxies that could produce a supernova inflationary explosion, or a deflationary black hole. We shall see – Japan perhaps will give us a glimpse into the global economy’s future, as to whether you can solve a debt crisis with more debt, or at least negative real interest rate debt.

And, as we learned last week, as if we didn’t know it before, each country has its own New Neutral policy rate that is not too hot / not too cold, but just right – and in our opinion lower than historic Neutrals because the world is now more highly levered. Mark Carney of the Bank of England will likely head the first of the G-7 countries to raise rates and explore where to stop at hopefully just the right spot. He will likely be the Christopher Columbus of G-7 central bankers, sailing upwards to find the East, and the wonderful spices of the U.K.’s New Neutral.

For now, however…investors must make choices, and simultaneously with this journey to The New Neutral, investors must be aware that QE, in the U.S. at least, will disappear as a policy choice in early November, and risk markets, including long-term Treasury bonds have feasted on that policy for 5 years now. What will happen when the Fed stops buying nearly 100% of all 30 year Treasuries being issued by their puppet counterparts – the U.S. Treasury? Talk about the left hand and the right hand – these days the Fed and the Treasury are nearly one and the same – one giant marionette. And that marionette, according to some (which includes PIMCO), has significantly fertilized risk assets including stocks. Is it a coincidence that stocks have doubled during the period of Quantitative Easing, while the Fed has injected 3.5 trillion dollars of checks into the credit markets? What will happen when the checks stop? We think, at the margin at least, that stock market appreciation will slow significantly and that credit spreads will stop tightening. And we assume that is what the Fed is hoping for too. But no bear markets if The New Neutral is closer to 0% than 2%.

But to the point – if The New Neutral is closer to 0% than 2% – if Taylor is replaced by PIMCO’s New Neutral – then risk assets, even without QE checks, can stand on their own two legs. They won’t be stilts, more like peg-legs in a historical context, but stable nonetheless. We expect bonds to return 3-4% over the next 5 years and stocks perhaps 4-5%. If central banks proceed cautiously, there’s no need for another Lehman Brothers, but as well, there will be no interest rate propellant for double-digit asset returns. Those days are gone. The journey to 0% nominal Fed Funds and a negative 1½% real rate is over. A 0% real Fed Funds New Neutral lies ahead, a tightening of credit yes, but a mild one to be sure.

And specifically what would PIMCO favor or recommend? Well, of the carry alternatives available to all investors we would favor credit and equity risk premiums (stocks) as well as volatility sales and the middle of the curve, as opposed to outright duration, although we would acknowledge, as I have, that the alpha heyday of all risk premiums is over. They are too tight to produce substantial capital gains, and their “carry” even when mildly levered lies in the 3-5% annual return range.

Big Idea Speed Read

1. The New Neutral is PIMCO’s one big idea currently.

2. If it is lower than the historical 2% real, and if it facilitates normal asset volatility, then stocks, bonds, and risk assets in general should appear less bubbly than some presume.

William H. Gross

Managing Director

Disclosures

All investments contain risk and may lose value. This material contains the current opinions of the author but not necessarily those of PIMCO and such opinions are subject to change without notice. This material is distributed for informational purposes only. Forecasts, estimates, and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark or registered trademark of Allianz Asset Management of America L.P. in the United States and throughout the world. THE NEW NEUTRAL and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Pacific Investment Management Company LLC in the United States and throughout the world. ©2014, PIMCO.