Recessions: What Investors Need to Know

- What is a recession?

- What factors cause a recession?

- How does a recession affect investment returns?

- What asset classes tend to do well in a recession?

- How can fixed income investors benefit from active management in a recession?

- What can investors do if they are worried about future recessions?

What Is A Recession?

A recession is a period of significant decline in economic activity that may last for months or years. Typically, a recession is marked by falling productivity, investments and business profits, as well as rising unemployment.Footnote1

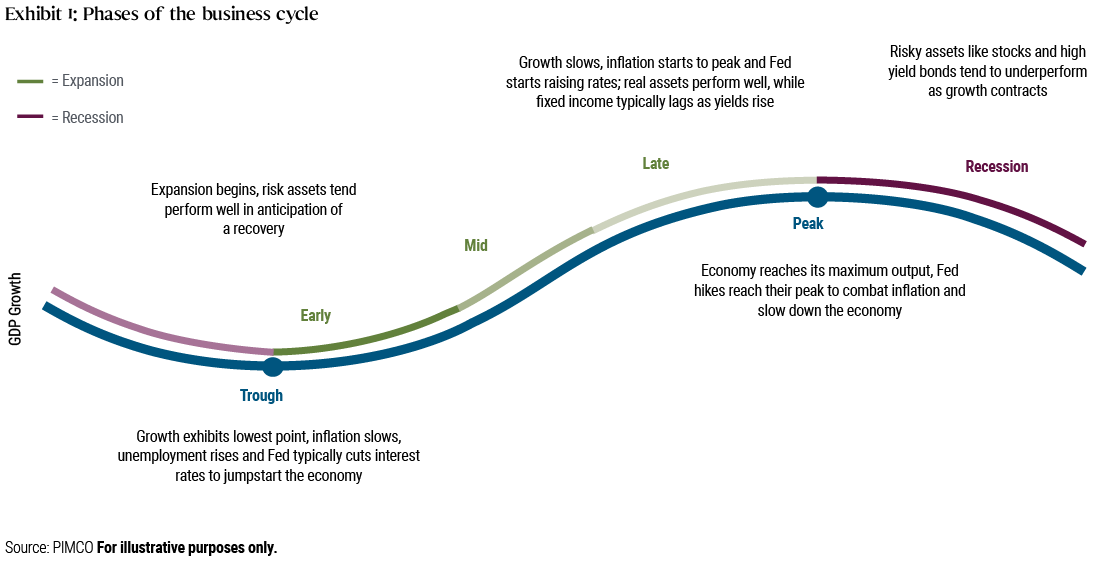

At any given time, the economy, which is made up of a country’s aggregate production and consumption, follows a pattern of activity often referred to as the business (or economic) cycle.

Consider the following: Footnote2

- Historically, recessions have been a natural part of the economic cycle, occurring every 3.25 years in the U.S.

- Between 1945 and 2019, the average U.S. recession lasted approximately 11 months, while the economic expansion that followed lasted an average of 65 months.

As Exhibit 1 shows, the business cycle starts during a period of economic growth, followed by a slowdown. After economic activity reaches its lowest point, or trough, it picks up again until it reaches its highest point. Once activity drops from the peak, this signals the start of a recessionary period.

What Factors Cause A Recession?Footnote3

The nature and causes of U.S. recessions have varied, and have been generally characterized by a decline in consumer and business spending. Consumer spending greatly affects economic activity, accounting for 68% of U.S. Gross Domestic Product (GDP).Footnote4

Some examples of the causes of recessions include:

- Unforeseen events – such as the 2020 COVID-19 global pandemic and geopolitical crises, which impacted supply chains and business activity

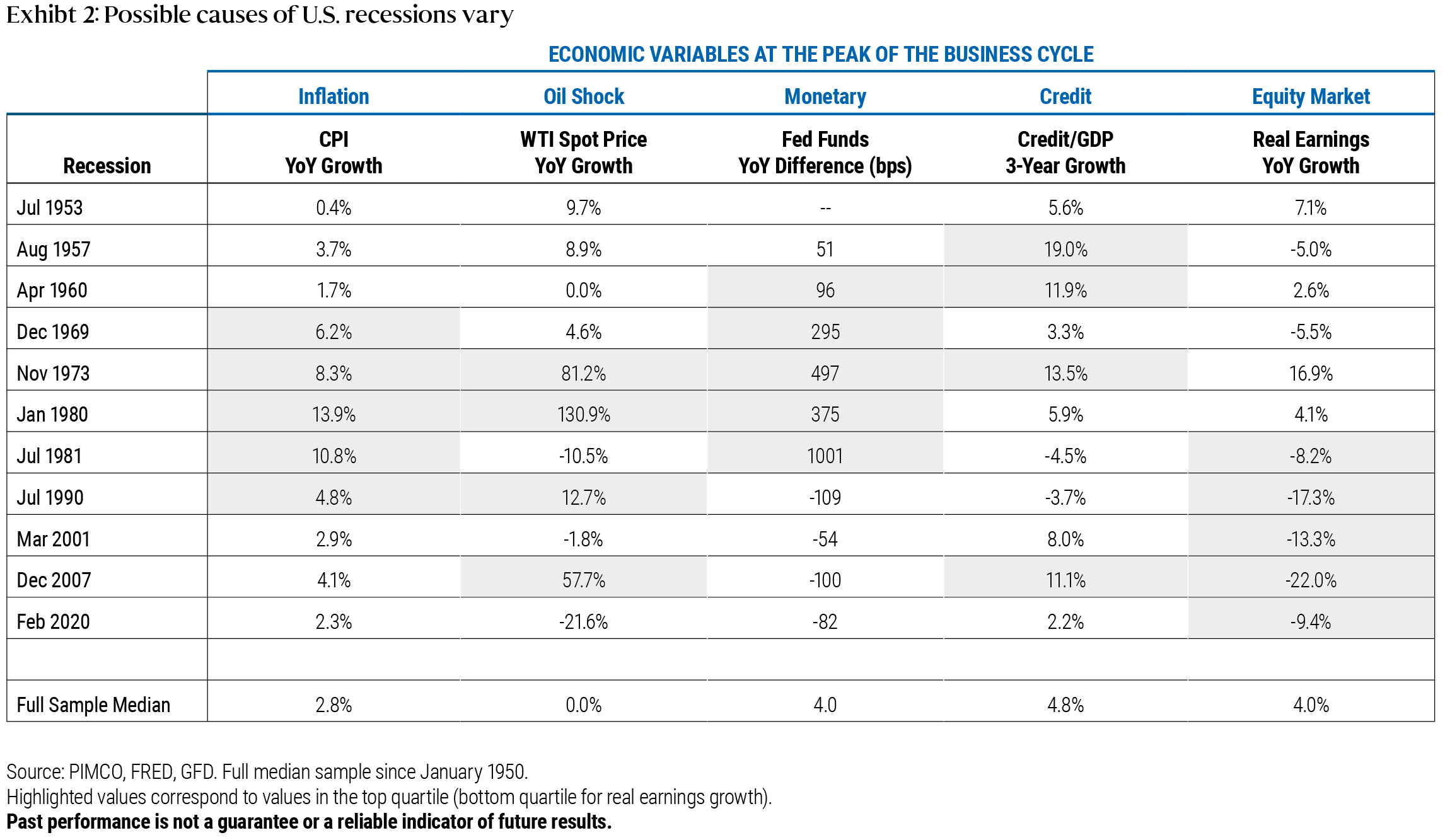

- Oil shocks/energy crises – rising oil prices in 1973 and 1980, which contributed to high inflation, as shown in Exhibit 2

- An overheated economy – characterized by low unemployment, rising inflation, and asset valuation bubbles, which may cause central banks worldwide to tighten financial conditions by raising short-term interest rates; examples of asset valuation bubbles that led to recessions included the dotcom bubble in 2001, and the real estate bubble that led to the 2008 Global Financial Crisis

Exhibit 2 shows U.S. recessions from the 1950s through 2020 and the various economic variables (measured at the peak of the business cycle) that contributed to recessions, including changes in inflation, oil prices, interest rates, credit/debt to GDP, and real (inflation-adjusted) corporate earnings.

The table’s shaded areas highlight the years with the highest increases for inflation, oil prices, interest rates, and credit/GDP, as well as the years with the steepest declines in real corporate earnings growth.

How Does A Recession Affect Investment Returns?

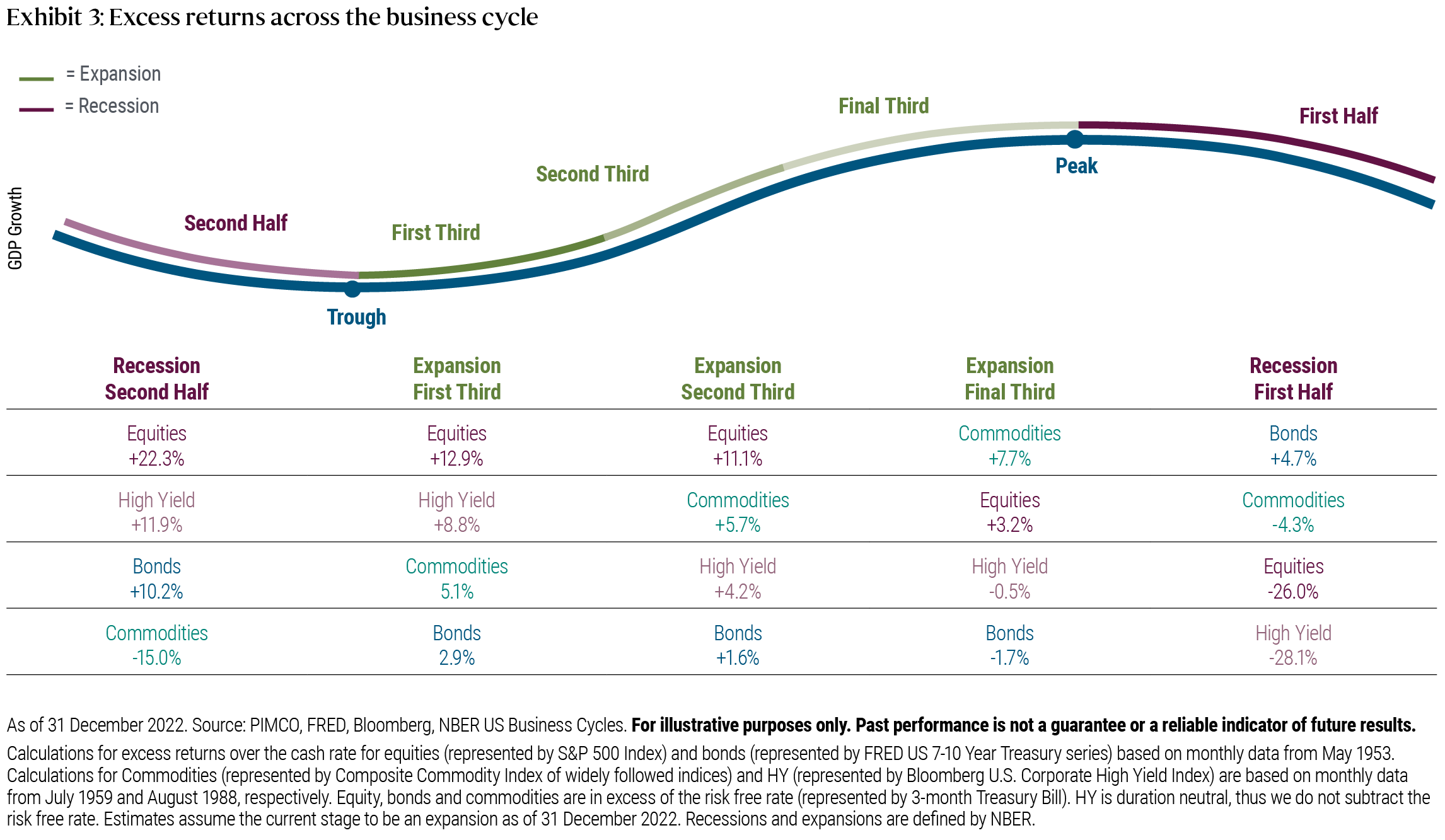

Exhibit 3 shows that recessionary periods have affected asset classes differently, with some outperforming others.

The first half of a recession (shown on the right) is typically marked by a decrease in economic activity from its late cycle stage “peak”, as measured by analyzing growth, inflation and unemployment data. During the first half of a recession stage, core bond returns (i.e., Treasuries and investment-grade securities) are historically positive, while returns for high yield bonds, equities, and commodities are negative.

The second half of a recession (shown on the left) is typically marked by a continued drop in economic activity – in which equities, high yield bonds, and core bonds historically perform well, and commodities decline – before the economy enters “recovery” or expansion stage (middle of chart).

What Asset Classes Tend To Do Well In A Recession?

In general, core bonds historically have tended to do well during recessions. Owning core bonds in all stages of the business cycle, and especially during an economic slowdown, may help investors preserve principal while reducing overall portfolio risk, as core bonds are typically less volatile than other asset classes.

Risk assets, such as equities, historically outperform during the second half of a recession and in the expansion phase.

The differences in returns highlight the importance of diversification, a strategy of allocating to various asset classes, which could enable investors to generate gains from some investments and help offset losses from others.

How Can Fixed Income Investors Benefit From Active Management In A Recession?

The bond market is vast and exceedingly diverse. It includes corporate and high yield bonds, mortgage-backed securities, municipal bonds, emerging market bonds, and more. Each sector or asset class responds differently to economic and market conditions.

Active fixed income managers typically have more flexibility than their passive peers to buy attractive securities and sell those that may underperform. For example, skilled active managers with robust credit research teams have resources to find attractive opportunities, and at the same time manage risks, across the global bond market.

What Can Investors Do If They Are Worried About Future Recessions?

Investors worried about a recession may benefit from taking the following steps to mitigate the potential impact on their portfolios:

- Avoid behavioral bias when making investment decisions such as selling low during market declines, and buying high during market upturns, which may lead to less than ideal long-term investment outcomes.

- Stay diversified to potentially mitigate portfolio volatility by allocating across different investments, such as equities, core bonds, credit, and alternatives.

- Ensure that your investment portfolio remains aligned with your long-term financial goals through regular rebalancing.

In summary, if there’s one important takeaway about recessions, it is that they are part of a vibrant economy. While they can be daunting and unpleasant in the short term, recessions may also present opportunities for patient, long-term investors.

GLOSSARYFootnote5

Basis Point: Equal to 1/100th of 1%.

Bonds: Fixed income investments representing a loan made by an investor to a borrower, such as a government or corporation.

Commodities: Basic goods used in commerce and can be traded with other types of goods. Commodities that can be traded in the public markets include energy, metals, livestock, and agriculture.

Consumer Price Index (CPI): Measures price changes for a representative basket of goods and services paid by consumers over time.

Consumer Spending: The total money spent on final goods and services by individuals and households.

Credit/Debt to GDP: Measures a country’s public debt to its gross domestic product (GDP).

Diversification: The strategy of spreading investments across various asset classes to help reduce portfolio volatility over time.

Dodd-Frank Wall Street Reform and Consumer Protection Act: Created in response to the financial crisis of 2007-2008, and was named after Senators Christopher Dodd and Barney Frank.

Equities: Shares of stock in a company.

Federal Funds Rate: The interest rates in which a depository institution lends funds maintained at the Fed to another depository institution overnight.

Federal Reserve (Fed): The U.S. central bank was created by Congress in 1913 to provide the nation with a safer, more flexible, and more stable monetary financial system. The Fed’s mandates include full employment and stable prices.Footnote6

Global Financial Crisis (GFC): The financial crisis of 2008, or GFC, marked a sharp decline in worldwide economic activity, triggered by the collapse of the U.S. housing market, which was fueled by low interest rates, easy credit, insufficient regulation, and toxic subprime mortgages.

Gross Domestic Product (GDP): The total market value of the goods and services produced within a country’s borders in a year. As a broad measure of overall domestic production, it functions as a comprehensive scorecard of a given country’s economic health.

High Yield Bonds: Debt securities issued by companies that can provide a higher yield than investment-grade bonds, but are considered riskier investments.

Inflation: The increase in the overall price of goods and services in an economy over time.

Investment-Grade Securities: Securities with investment grade ratings that fall within the range of Aaa to Baa3 from credit rating agencies Moody’s, or AAA to BBB-from Standard & Poor’s. A company’s securities have investment grade ratings if it has a strong capacity to meet its financial commitments.

Monetary Policy: A set of tools used by a nation’s central bank to control the overall money supply and promote economic growth. These tools include changing the level of interest rates and bank-reserve requirements.

National Bureau of Economic Research (NBER): A non-profit organization that tracks economic growth and retroactively declares recession periods in the United States.

Treasuries: U.S. Treasury securities issued by the federal government and are considered to be among the safest investments, because all Treasury securities are backed by the “full faith and credit” of the U.S. government.

Volatility: A measure of price fluctuations for securities, derivatives, and market indices.

West Texas Intermediate (WTI): The benchmark crude of the U.S. oil industry.

Yield Curve: A line that plots interest rates, at a set point in time, of bonds having equal credit quality but different maturity.

Download PDF

Disclosures

1 National Bureau of Economic Research “Business Cycle Dating” https://www.nber.org/research/business-cycle-dating#:~:text=The%20NBER's%20definition%20emphasizes%20that,more%20than%20a%20few%20months. Federal Reserve Bank of St. Louis “Is the U.S. in a Recession? What Key Economic Indicators Say” Sept. 26, 2022 https://www.stlouisfed.org/en/on-the-economy/2022/sep/us-recession-what-key-economic-indicators-say Return to content

2 Kiplinger “What is a Recession? 10 Facts You Need to Know” November 22, 2022; Congressional Research Service “Introduction to U.S. Economy: The Business Cycle and Growth” January 3, 2023 Return to content

3 PIMCO and Federal Reserve Economic Data – Federal Reserve Bank of St. Louis; Federal Reserve Bank of St. Louis Economic Research, March 2023 https://research.stlouisfed.org/publications/page1-econ/2023/03/01/all-about-the-business-cycle-where-do-recessions-come-from Return to content

4 Federal Reserve Bank of St. Louis “Shares of gross domestic product: Personal Consumption Expenditures” Q1 2023 https://fred.stlouisfed.org/series/DPCERE1Q156NBEA Return to content

5 (various terms and definitions) GLOSSARY Bureau of Economic Analysis, U.S. Department of Commerce https://www.bea.gov/ ; Federal Reserve https://www.federalreserve.gov/faqs.htm; Investopedia https://www.investopedia.com/ ; FINRA https://www.finra.org/investors/learn-to-invest/types-investments/bonds/types-of-bonds/us-treasury-securities; CME Group https://www.cmegroup.com/education/glossary.html#WReturn to content

6 Board of Governors of the Federal Reserve System FAQs “What is the purpose of the Federal Reserve System?” https://www.federalreserve.gov/faqs/about_12594.htm Return to content

Past performance is not a guarantee or a reliable indicator of future results.

Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be appropriate for all investors. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Investing in foreign denominated and/or domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Mortgage and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and their value may fluctuate in response to the market’s perception of issuer creditworthiness; while generally supported by some form of government or private guarantee there is no assurance that private guarantors will meet their obligations. High-yield, lower-rated, securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not. Diversification does not ensure against loss.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

S&P 500 Index is an unmanaged market index generally considered representative of the stock market as a whole. The Index focuses on the large-cap segment of the U.S. equities market. The Bloomberg U.S. Corporate High-Yield Index the covers the USD-denominated, non-investment grade, fixed-rate, taxable corporate bond market. Securities are classified as high-yield if the middle rating of Moody’s, Fitch, and S&P is Ba1/BB+/BB+ or below. The index excludes Emerging Markets debt. FRED, short for Federal Reserve Economic Data, is an online database of economic data time series created and maintained by the Research Department at the Federal Reserve Bank of St. Louis. It is not possible to invest directly in an unmanaged index.

This material contains the current opinions of the manager but not necessarily those of PIMCO] and such opinions are subject to change without notice. This material is distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This is not an offer to any person in any jurisdiction where unlawful or unauthorized. | Pacific Investment Management Company LLC, 650 Newport Center Drive, Newport Beach, CA 92660 is regulated by the United States Securities and Exchange Commission. | PIMCO Europe Ltd (Company No. 2604517, 11 Baker Street, London W1U 3AH, United Kingdom) is authorised and regulated by the Financial Conduct Authority (FCA) (12 Endeavour Square, London E20 1JN) in the UK. The services provided by PIMCO Europe Ltd are not available to retail investors, who should not rely on this communication but contact their financial adviser. | PIMCO Europe GmbH (Company No. 192083, Seidlstr. 24-24a, 80335 Munich, Germany), PIMCO Europe GmbH Italian Branch (Company No. 10005170963, Corso Vittorio Emanuele II, 37/Piano 5, 20122 Milano, Italy), PIMCO Europe GmbH Irish Branch (Company No. 909462, 57B Harcourt Street Dublin D02 F721, Ireland), PIMCO Europe GmbH UK Branch (Company No. FC037712, 11 Baker Street, London W1U 3AH, UK), PIMCO Europe GmbH Spanish Branch (N.I.F. W2765338E, Paseo de la Castellana 43, Oficina 05-111, 28046 Madrid, Spain) and PIMCO Europe GmbH French Branch (Company No. 918745621 R.C.S. Paris, 50–52 Boulevard Haussmann, 75009 Paris, France) are authorised and regulated by the German Federal Financial Supervisory Authority (BaFin) (Marie- Curie-Str. 24-28, 60439 Frankfurt am Main) in Germany in accordance with Section 15 of the German Securities Institutions Act (WpIG). The Italian Branch, Irish Branch, UK Branch, Spanish Branch and French Branch are additionally supervised by: (1) Italian Branch: the Commissione Nazionale per le Società e la Borsa (CONSOB) (Giovanni Battista Martini, 3 - 00198 Rome) in accordance with Article 27 of the Italian Consolidated Financial Act; (2) Irish Branch: the Central Bank of Ireland (New Wapping Street, North Wall Quay, Dublin 1 D01 F7X3) in accordance with Regulation 43 of the European Union (Markets in Financial Instruments) Regulations 2017, as amended; (3) UK Branch: the Financial Conduct Authority (FCA) (12 Endeavour Square, London E20 1JN); (4) Spanish Branch: the Comisión Nacional del Mercado de Valores (CNMV) (Edison, 4, 28006 Madrid) in accordance with obligations stipulated in articles 168 and 203 to 224, as well as obligations contained in Tile V, Section I of the Law on the Securities Market (LSM) and in articles 111, 114 and 117 of Royal Decree 217/2008, respectively and (5) French Branch: ACPR/Banque de France (4 Place de Budapest, CS 92459, 75436 Paris Cedex 09) in accordance with Art. 35 of Directive 2014/65/EU on markets in financial instruments and under the surveillance of ACPR and AMF. The services provided by PIMCO Europe GmbH are available only to professional clients as defined in Section 67 para. 2 German Securities Trading Act (WpHG). They are not available to individual investors, who should not rely on this communication. | PIMCO (Schweiz) GmbH (registered in Switzerland, Company No. CH-020.4.038.582-2, Brandschenkestrasse 41 Zurich 8002, Switzerland). The services provided by PIMCO (Schweiz) GmbH are not available to retail investors, who should not rely on this communication but contact their financial adviser. | PIMCO Asia Pte Ltd (Registration No. 199804652K) is regulated by the Monetary Authority of Singapore as a holder of a capital markets services licence and an exempt financial adviser. The asset management services and investment products are not available to persons where provision of such services and products is unauthorised. | PIMCO Asia Limited is licensed by the Securities and Futures Commission for Types 1, 4 and 9 regulated activities under the Securities and Futures Ordinance. PIMCO Asia Limited is registered as a cross-border discretionary investment manager with the Financial Supervisory Commission of Korea (Registration No. 08-02-307). The asset management services and investment products are not available to persons where provision of such services and products is unauthorised. | PIMCO Investment Management (Shanghai) Limited. Office address: Suite 7204, Shanghai Tower, 479 Lujiazui Ring Road, Pudong, Shanghai 200120, China (Unified social credit code: 91310115MA1K41MU72) is registered with Asset Management Association of China as Private Fund Manager (Registration No. P1071502, Type: Other). | PIMCO Australia Pty Ltd ABN 54 084 280 508, AFSL 246862. This publication has been prepared without taking into account the objectives, financial situation or needs of investors. Before making an investment decision, investors should obtain professional advice and consider whether the information contained herein is appropriate having regard to their objectives, financial situation and needs. | PIMCO Japan Ltd, Financial Instruments Business Registration Number is Director of Kanto Local Finance Bureau (Financial Instruments Firm) No. 382. PIMCO Japan Ltd is a member of Japan Investment Advisers Association, The Investment Trusts Association, Japan and Type II Financial Instruments Firms Association. All investments contain risk. There is no guarantee that the principal amount of the investment will be preserved, or that a certain return will be realized; the investment could suffer a loss. All profits and losses incur to the investor. The amounts, maximum amounts and calculation methodologies of each type of fee and expense and their total amounts will vary depending on the investment strategy, the status of investment performance, period of management and outstanding balance of assets and thus such fees and expenses cannot be set forth herein. | PIMCO Taiwan Limited is an independently operated and managed company. The reference number of business license of the company approved by the competent authority is (112) Jin Guan Tou Gu Xin Zi No. 012. The registered address of the company is 40F., No.68, Sec. 5, Zhongxiao East Rd., Xinyi District, Taipei City 110, Taiwan (R.O.C.), and the telephone number is +886 2 8729-5500. | PIMCO Canada Corp. (199 Bay Street, Suite 2050, Commerce Court Station, P.O. Box 363, Toronto, ON, M5L 1G2) services and products may only be available in certain provinces or territories of Canada and only through dealers authorized for that purpose. | PIMCO Latin America Av. Brigadeiro Faria Lima 3477, Torre A, 5° andar São Paulo, Brazil 04538-133. | No part of this publication may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world. © 2023, PIMCO.

CMR2023-0717-2999196