Inflation-Linked Bonds (ILBs)

- Bonds: An instrument of debt issued by a corporation or government to raise capital. Bonds are interest bearing and promise to pay the holder a specified sum of money at its maturity plus interest at given intervals.

- Breakeven inflation rate: The difference between real yields and nominal yields.

- Commodities: A commodity is food, metal, or another fixed physical substance that investors buy or sell, usually via futures contracts.

- Correlation: A statistical measure of how two securities, such as equities, bonds, commodities, move in relation to each other.

- Diversification: A risk management technique that mixes a wide variety of investments within a portfolio. The rationale behind this technique contends that a portfolio of different kinds of investments will, on average, yield higher returns and pose a lower risk than any individual investment found within the portfolio.

- Equities: Ownership or proprietary rights and interests in a company – synonymous with equities.

- Maturity: The date on which a loan, bond, mortgage or other debt security becomes due and is to be paid off.

- Nominal yields: The rate listed on the face of a bond; the coupon rate.

- Real yields: The nominal yield, or rate listed on the face of a bond, minus the rate of inflation.

- Risk-adjusted returns: The return your investment has made relative to the amount of risk the investment has taken over a given period of time.

What is the impact of inflation on an investment portfolio?

Inflation is an economic term that describes the general rise in prices of consumer goods and services. As prices rise, a dollar saved buys less goods and services, or in other words, investors lose purchasing power of their dollar. To account for the effects of inflation, investors should focus on “real” return - the amount earned after adjusting for inflation. Investments that target returns above the rate of inflation can protect and potentially increase investors’ future purchasing power.

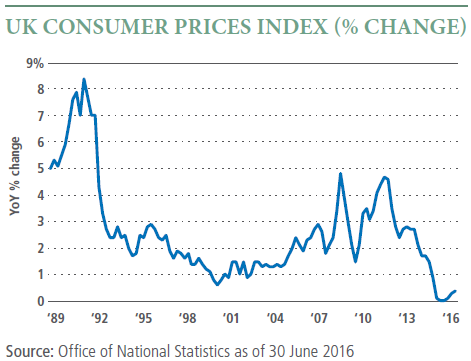

Global inflation has been falling since the early 1990s. Over the last decade in the UK, the Consumer Prices Index (CPI) has been between two and three percent, which is broadly in line with the Bank of England’s inflation target. Yet even at a relatively low rate of 2.5%, a basket of goods and services that cost £100 ten years ago would cost £128 today. This illustrates how inflation erodes purchasing power over time.

The effect of inflation on investment returns can be just as destructive. Assume a hypothetical equity portfolio return of 4% per year and an inflation rate of 2.5%. The real return of this portfolio, or the return minus the rate of inflation, would be 1.5%. So, in this case, an investment in equities would increase investors’ purchasing power by only 1.5% a year. An investment in a GBP money market fund, savings account or any other investment returning less than the 2.5% rate of inflation would effectively erode purchasing power, defeating even the most conservative goal of maintaining quality of life.

What are inflation-linked bonds, or ILBs?

Inflation-linked bonds are designed to help protect investors from the negative impact of inflation by contractually linking the bonds’ principal and interest payments to a nationally recognized inflation measure such as the Retail Price Index (RPI) in the UK, the European Harmonised Index of Consumer Prices (HICP) ex-tobacco in Europe, and the Consumer Price Index (CPI) in the U.S.

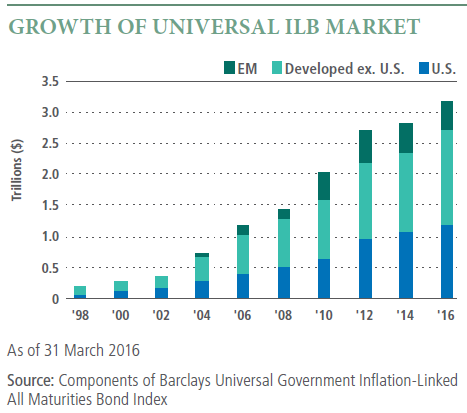

The earliest recorded inflation-indexed bonds were issued by the Commonwealth of Massachusetts in 1780 during the Revolutionary War. Much later, emerging market countries began issuing ILBs in the 1960s. In the 1980s, the UK was the first major developed market to introduce “linkers” to the market. Several other countries followed, including Australia, Canada, Mexico and Sweden. In January 1997, the U.S. began issuing Treasury Inflation-Protected Securities (TIPS), now the largest component of the global ILB market. Today inflation-linked bonds are typically sold by governments in an effort to reduce borrowing costs and broaden their investor base. Corporations have occasionally issued inflation-linked bonds for the same reasons, but the total amount has been relatively small.

How do ILBs work?

An ILB’s explicit link to a nationally-recognized inflation measure means that any increase in price levels directly translates into higher principal values. As a hypotheticalexample, consider a $1,000 20-year U.S. TIPS with a 2.5% coupon (1.25% on semiannual basis), and an inflation rate of 4%. The principal on the TIPS note will adjust upward on a daily basis to account for the 4% inflation rate. At maturity, the principal value will be $2,208 (4% per year, compounded semiannually). Additionally, while the coupon rate remains fixed at 2.5%, the dollar value of each interest payment will rise, as the coupon will be paid on the inflation-adjusted principal value. The first semiannual coupon of 1.25% paid on the inflation-adjusted principal of $1,020 is $12.75, while the final semiannual interest payment will be 1.25% of $2,208, which is $27.60.

While the exact mechanism for calculating payments can differ across specific issuers, all ILBs are designed to provide investors with returns contractually linked to inflation that may be used as a tool to hedge against rising price levels.

The inflation hedge offered by ILBs is important because every investor and consumer is exposed to inflation, and should consider having some measure of inflation protection in their portfolio. Since traditional asset classes such as stocks and bonds - which tend to dominate many portfolios - can be adversely affected by periods of persistent inflation, ILBs, with their explicit link to changes in inflation, are an effective way to incorporate explicit real returns into a portfolio.

What factors affect the performance and risks of ILBs?

Together with inflation accrual and coupon payments, the third driver of ILBs’ total return comes from the price fluctuation due to changes in real yields. If the bond is held to maturity, the price change component becomes irrelevant; however, prior to expiration, the market value of the bond moves higher or lower than its par amount.

Just like nominal bonds,whose prices move in response to nominal interest rate changes, ILB prices will increase as real yields decline and decrease as real yields rise. Should an economy undergo a period of deflation – a sustained decline in price levels during the life of an ILB, the inflation-adjusted principal could decline below its par value. Subsequently, coupon payments would be based on this deflation-adjusted amount. However, many ILB-issuing countries, such as the U.S., Australia, France and Germany, offer deflation floors at maturity: if deflation drives the principal amount below par, an investor would still receive the full par amount at maturity. So, while coupon payments are paid on a principal adjusted for inflation or deflation, an investor receives the greater of the inflation-adjusted principal or the initial par amount at maturity.

How do I determine the relative value of ILBs?

To compare ILBs with nominal government bonds and determine their relative value, investors can look at the difference between nominal yields and real yields, called the breakeven inflation rate. The difference indicates the inflation expectations priced into the market; it is the rate differential at which the expected returns of ILBs and nominal bonds are equal. If the actual inflation rate over the life of the bond is higher than the breakeven inflation rate, investors would earn a higher return holding ILBs while having lower inflation risk.

If the actual inflation rate is lower than expectations, the nominal bond of the same maturity would garner a higher return, though with a higher inflation risk. For example, if a 10-year nominal UK gilt is yielding 2.5% and a 10-year UK inflation-linked bond is yielding 0.25%, then the breakeven inflation rate is 2.25%. If an investor believes the UK inflation rate will be above 2.25% for the next 10 years, then a then an Inflation-Linked Bond would be a more attractive investment.

What are the risks?

As with other investments, the price of ILBs can fluctuate, and if real yields rise, the market value of an ILB will fall. Real yields can rise, without a corresponding increase in nominal yields. If held to maturity however, the market value fluctuations are irrelevant and an investor receives the par amount. In theory, a period of deflation could reduce this par amount. However, in practice most ILBs are issued with a deflation floor to mitigate this risk.

Disclosures

Past performance is not a guarantee or a reliable indicator of future results.

A word about risk: All investments contain risk and can lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be appropriate for all investors. Inflation-linked bonds (ILBs) issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. Treasury Inflation-Protected Securities (TIPS) are ILBs issued by the U.S. government. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Management risk is the risk that the investment techniques and risk analyses applied by PIMCO will not produce the desired results, and that certain policies or developments may affect the investment techniques available to PIMCO in connection with managing the strategy. Diversification does not ensure against loss.

HYPOTHETICAL PERFORMANCE RESULTS HAVE MANY INHERENT LIMITATIONS, SOME OF WHICH ARE DESCRIBED BELOW. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES SIMILAR TO THOSE SHOWN. IN FACT, THERE ARE FREQUENTLY SHARP DIFFERENCES BETWEEN HYPOTHETICAL PERFORMANCE RESULTS AND THE ACTUAL RESULTS SUBSEQUENTLY ACHIEVED BY ANY PARTICULAR TRADING PROGRAM.

ONE OF THE LIMITATIONS OF HYPOTHETICAL PERFORMANCE RESULTS IS THAT THEY ARE GENERALLY PREPARED WITH THE BENEFIT OF HINDSIGHT. IN ADDITION, HYPOTHETICAL TRADING DOES NOT INVOLVE FINANCIAL RISK, AND NO HYPOTHETICAL TRADING RECORD CAN COMPLETELY ACCOUNT FOR THE IMPACT OF FINANCIAL RISK IN ACTUAL TRADING. FOR EXAMPLE, THE ABILITY TO WITHSTAND LOSSES OR TO ADHERE TO A PARTICULAR TRADING PROGRAM IN SPITE OF TRADING LOSSES ARE MATERIAL POINTS WHICH CAN ALSO ADVERSELY AFFECT ACTUAL TRADING RESULTS. THERE ARE NUMEROUS OTHER FACTORS RELATED TO THE MARKETS IN GENERAL OR TO THE IMPLEMENTATION OF ANY SPECIFIC TRADING PROGRAM WHICH CANNOT BE FULLY ACCOUNTED FOR IN THE PREPARATION OF HYPOTHETICAL PERFORMANCE RESULTS AND ALL OF WHICH CAN ADVERSELY AFFECT ACTUAL TRADING RESULTS.

There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market.

The Consumer Price Index (CPI) is an unmanaged index representing the rate of inflation of the U.S. consumer prices as determined by the U.S. Department of Labor Statistics. There can be no guarantee that the CPI or other indexes will reflect the exact level of inflation at any given time. It is not possible to invest directly in an unmanaged index.

This material contains the current opinions of the manager and such opinions are subject to change without notice. This material is distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This is not an offer to any person in any jurisdiction where unlawful or unauthorized. | Pacific Investment Management Company LLC, 650 Newport Center Drive, Newport Beach, CA 92660 is regulated by the United States Securities and Exchange Commission. | PIMCO Europe Ltd (Company No. 2604517) and PIMCO Europe Ltd - Italy (Company No. 07533910969) are authorised and regulated by the Financial Conduct Authority (12 Endeavour Square, London E20 1JN) in the UK. The Italy branch is additionally regulated by the Commissione Nazionale per le Società e la Borsa (CONSOB) in accordance with Article 27 of the Italian Consolidated Financial Act. PIMCO Europe Ltd services are available only to professional clients as defined in the Financial Conduct Authority’s Handbook and are not available to individual investors, who should not rely on this communication. | PIMCO Deutschland GmbH (Company No. 192083, Seidlstr. 24-24a, 80335 Munich, Germany), PIMCO Deutschland GmbH Italian Branch (Company No. 10005170963) and PIMCO Deutschland GmbH Spanish Branch (N.I.F. W2765338E) are authorised and regulated by the German Federal Financial Supervisory Authority (BaFin) (Marie- Curie-Str. 24-28, 60439 Frankfurt am Main) in Germany in accordance with Section 32 of the German Banking Act (KWG). The Italian Branch and Spanish Branch are additionally supervised by the Commissione Nazionale per le Società e la Borsa (CONSOB) in accordance with Article 27 of the Italian Consolidated Financial Act and the Comisión Nacional del Mercado de Valores (CNMV) in accordance with obligations stipulated in articles 168 and 203 to 224, as well as obligations contained in Tile V, Section I of the Law on the Securities Market (LSM) and in articles 111, 114 and 117 of Royal Decree 217/2008, respectively. The services provided by PIMCO Deutschland GmbH are available only to professional clients as defined in Section 67 para. 2 German Securities Trading Act (WpHG). They are not available to individual investors, who should not rely on this communication. | PIMCO (Schweiz) GmbH (registered in Switzerland, Company No. CH-020.4.038.582-2), Brandschenkestrasse 41, 8002 Zurich, Switzerland, Tel: + 41 44 512 49 10. The services provided by PIMCO (Schweiz) GmbH are not available to individual investors, who should not rely on this communication but contact their financial adviser. | PIMCO Asia Pte Ltd (Registration No. 199804652K) is regulated by the Monetary Authority of Singapore as a holder of a capital markets services licence and an exempt financial adviser. The asset management services and investment products are not available to persons where provision of such services and products is unauthorised. | PIMCO Asia Limited is licensed by the Securities and Futures Commission for Types 1, 4 and 9 regulated activities under the Securities and Futures Ordinance. PIMCO Asia Limited is registered as a cross-border discretionary investment manager with the Financial Supervisory Commission of Korea (Registration No. 08-02-307). The asset management services and investment products are not available to persons where provision of such services and products is unauthorised. | PIMCO Australia Pty Ltd ABN 54 084 280 508, AFSL 246862. This publication has been prepared without taking into account the objectives, financial situation or needs of investors. Before making an investment decision, investors should obtain professional advice and consider whether the information contained herein is appropriate having regard to their objectives, financial situation and needs. | PIMCO Japan Ltd, Financial Instruments Business Registration Number is Director of Kanto Local Finance Bureau (Financial Instruments Firm) No. 382. PIMCO Japan Ltd is a member of Japan Investment Advisers Association and The Investment Trusts Association, Japan. All investments contain risk. There is no guarantee that the principal amount of the investment will be preserved, or that a certain return will be realized; the investment could suffer a loss. All profits and losses incur to the investor. The amounts, maximum amounts and calculation methodologies of each type of fee and expense and their total amounts will vary depending on the investment strategy, the status of investment performance, period of management and outstanding balance of assets and thus such fees and expenses cannot be set forth herein. | PIMCO Taiwan Limited is managed and operated independently. The reference number of business license of the company approved by the competent authority is (107) FSC SICE Reg. No.001. 40F., No.68, Sec. 5, Zhongxiao E. Rd., Xinyi Dist., Taipei City 110, Taiwan (R.O.C.), Tel: +886 2 8729-5500. | PIMCO Canada Corp. (199 Bay Street, Suite 2050, Commerce Court Station, P.O. Box 363, Toronto, ON, M5L 1G2) services and products may only be available in certain provinces or territories of Canada and only through dealers authorized for that purpose. | PIMCO Latin America Av. Brigadeiro Faria Lima 3477, Torre A, 5° andar São Paulo, Brazil 04538-133. | No part of this publication may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world. ©2020, PIMCO.